Looking ahead: key digital themes for 2023

DataReportal’s Simon Kemp recently hosted a livestream to share a selection of digital trends and themes that will shape marketing success in 2023 and beyond.

You can watch the presentation that Simon delivered during that livestream in the YouTube embed below, but scroll on past that to find the complete slide deck that Simon used in his presentation, and a full transcript of the video’s talk track.

Note that digital trends change quickly though, so if you’re watching this after October 2022, be sure to check our complete online library to find the very latest insights into evolving digital behaviours in every country in the world.

The presentation: what 2023 holds

Click here if you can’t see the YouTube video embed below

The complete set of presentation slides

Click here if you can’t see the SlideShare embed below.

Digging deeper: what 2023 holds

The remainder of this article contains a text version of the talk track in Simon’s presentation.

So welcome everybody, and thanks very much for joining today’s look ahead to some of the key digital themes for 2023.

Just in case we’ve not met before, hello! I’m Simon Kemp, and I run a management advisory company called Kepios, that helps the world make sense of what people are really doing online.

And a big part of our work centres on our Global Digital Reports series, which we publish in partnership with We Are Social and Hootsuite.

But the good news is that I’m not here to sell you anything today…

Instead, I’ll be exploring the key trends and themes that we believe will shape the world of digital in 2023 and beyond.

And we’ve got loads to cover today, so let’s dive straight in, starting with a look at the latest digital headlines.

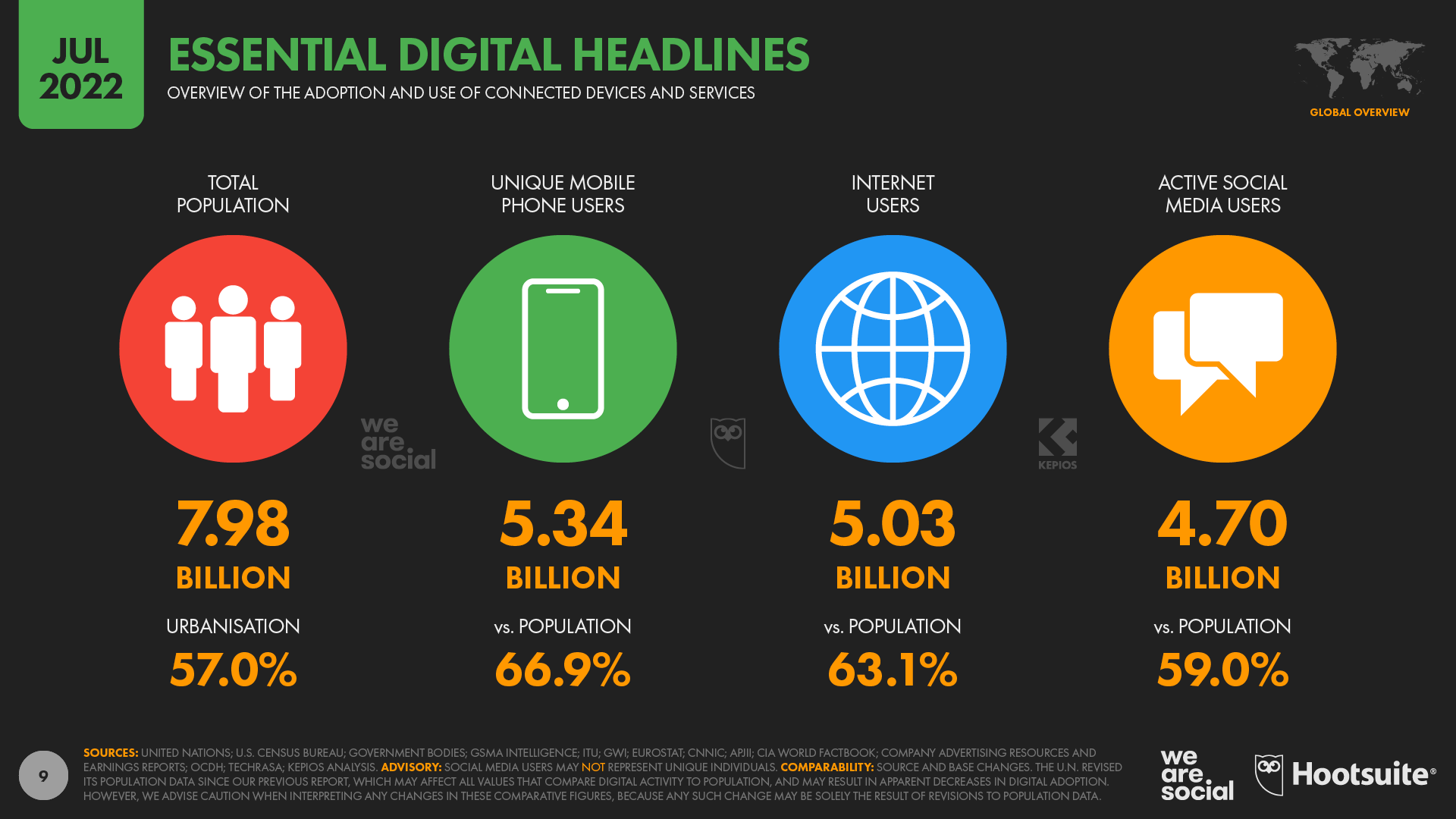

And as you can see from the numbers on this chart, digital adoption has already reached impressive levels around the world.

There are now more than 5 billion people using the internet, and social media users have just reached the 4.7 billion mark.

Our ongoing research shows that these numbers are still growing too, with almost 200 million people coming online for the first time in the 12 months to July 2022.

However, regular readers of our Global Digital Reports might notice that these latest numbers are quite a bit lower than the growth figures we reported at the height of COVID-19 lockdowns, and that brings us neatly to our first key theme for 2023.

#1: The outlook for digital growth

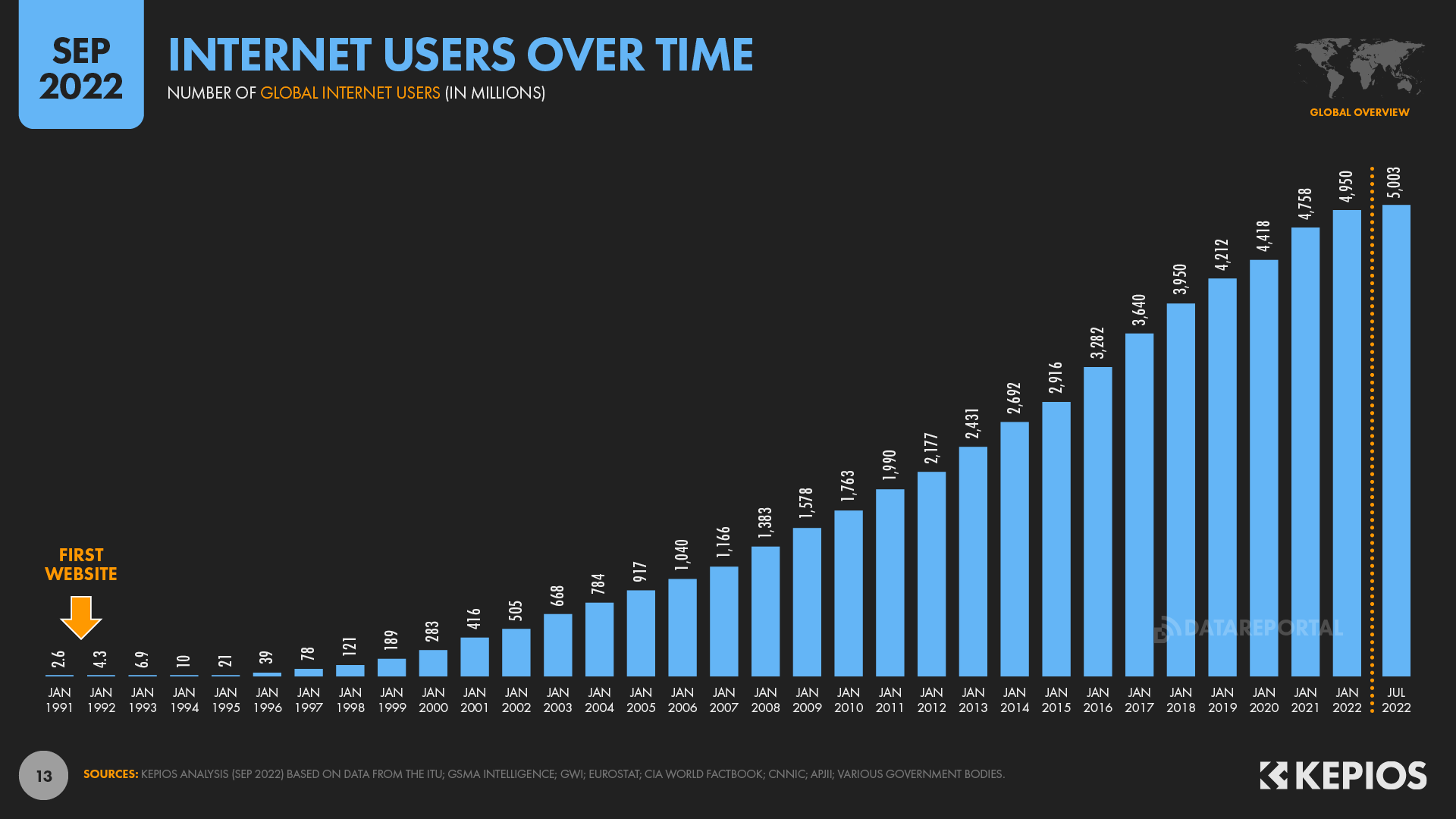

Now, as you can see on the chart here, it only took about 30 years from the time when Tim Berners-Lee brought us the first website, to the point where more than 5 billion people were online.

And at current rates, we can expect roughly two-thirds of the world’s total population to be online by the end of 2023.

That means that – by the end of next year – the internet will reach roughly the same number of people as television.

For context, Statista reports that TV reaches an audience of roughly 5.41 billion people today, compared with an audience of slightly over 5 billion people for connected tech.

However, with internet users continuing to grow much faster than the global TV audience, these two numbers should be roughly equal within the next 18 months.

Meanwhile, Kepios analysis suggests that more than three-quarters of all eligible audiences aged 13-plus already use social media today, and we’re on track for the global social media user total to reach 5 billion by the end of next year.

However, it’s important to recognise that it’s becoming increasingly difficult to “connect” those people who remain offline.

Now, it’s unlikely that we’d ever reach universal internet connectivity, partly because there will always be some people who choose to remain offline.

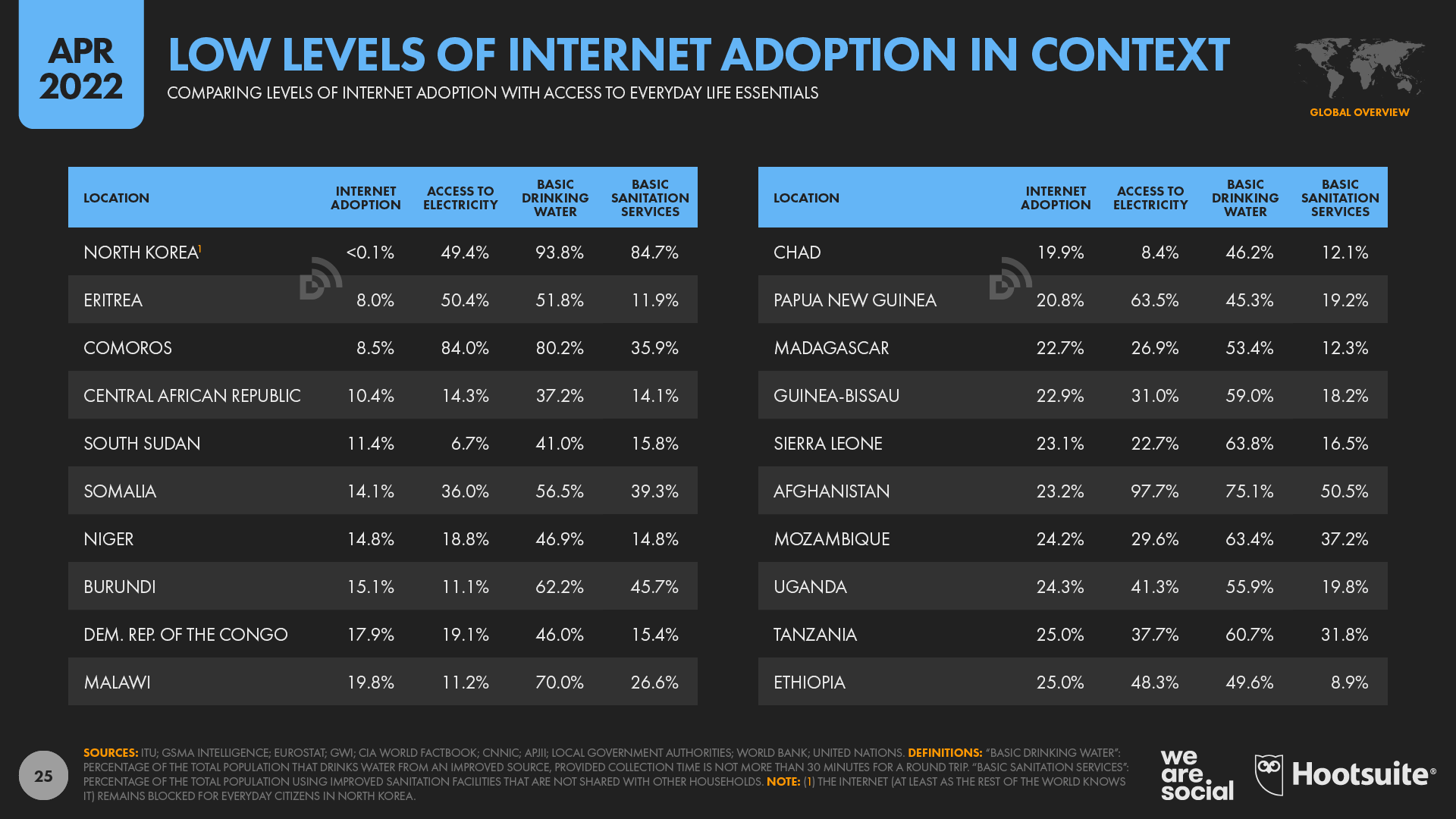

However, there are still various barriers preventing billions of people who do want to use the internet from coming online.

For example, in many parts of the world, less than half of the population currently has access to electricity, and in South Sudan, that figure is barely 1 in 15 people.

Meanwhile, hundreds of millions of people still need to walk more than half an hour to access basic drinking water, so it’s clear that there are other, far more important challenges to address before we can bring these populations online.

As a result of these challenges, we expect to see digital user growth rates slow from here on, especially compared with some of the more elevated growth rates we saw during the height of the pandemic.

But it’s not just user growth rates that have slowed.

#2: The time people spend online

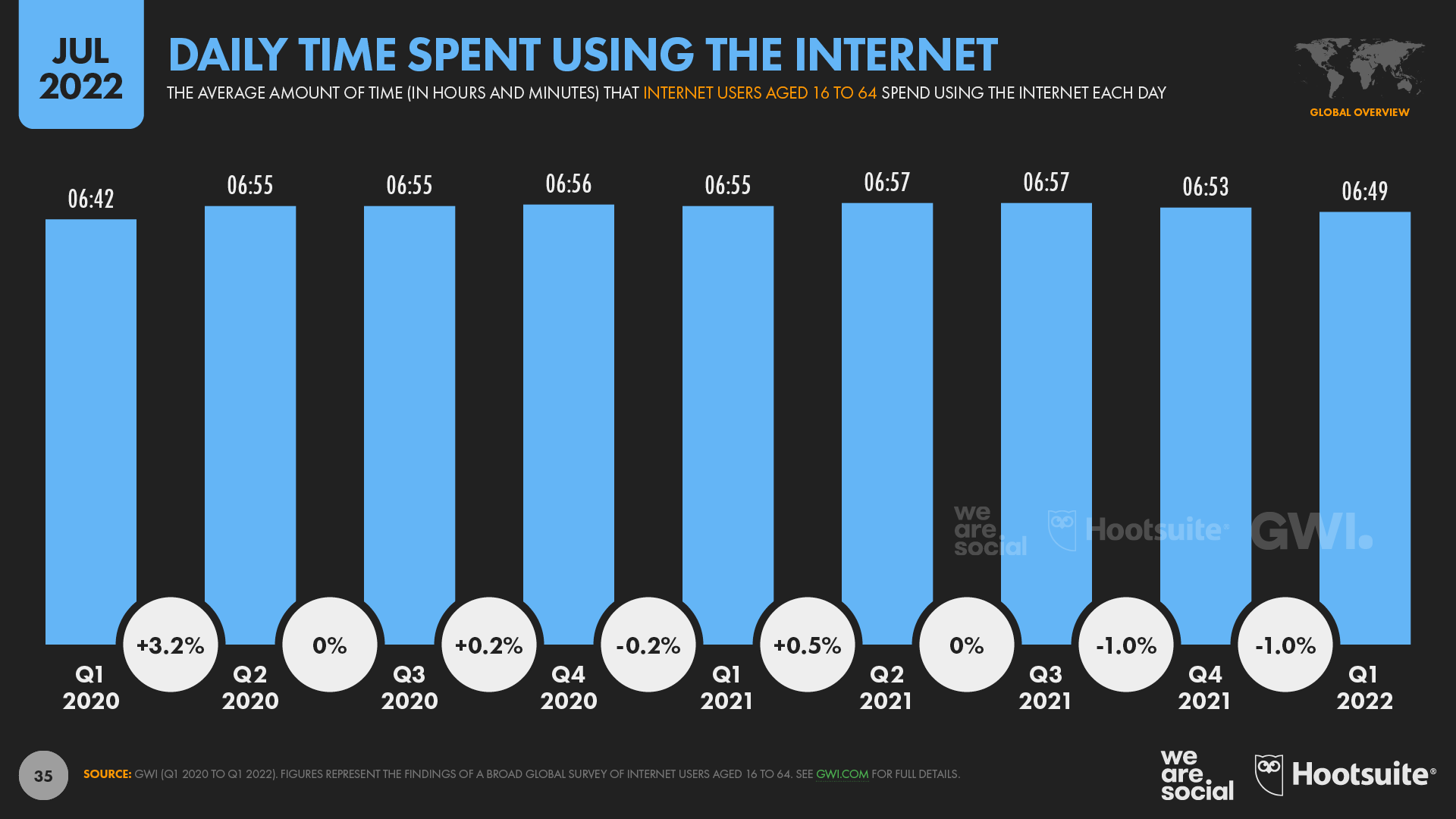

On average, the typical internet user now spends more than 40 percent of their waking life using connected devices and services.

And that means that the world’s internet population will spend a combined total of more than 1.4 billion years of collective human existence using the internet in 2022 alone.

However, the amount of time that each individual spends online has remained relatively stable over recent years, and in fact, we’ve seen the global average fall slightly over recent months.

As a result, when people adopt new digital activities, those new activities are increasingly taking time away from existing digital activities, rather than taking time away from offline media like print or TV.

And this means that – in order to ensure enduring success and growth – connected services need to place greater emphasis on delivering enduring value to their users, rather than prioritising massive scale.

And this has particular relevance to services that rely on interruptive advertising.

As people become increasingly conscious of how and where they spend their time online, they’re likely to become more sensitive to irritations, and especially to the sense that they may be wasting their time by watching interruptive ads.

#3: Rethinking how we see social media platforms

Now, as you can imagine, this would have particular relevance to social media platforms, so let’s take a closer look at some changes in people’s social media activities.

And the first thing to note here is that – as with our total online time – the amount of time that people say they spend using social media services has remained relatively stable over the past couple of years.

But what’s interesting here is that the mix of platforms that capture the greatest share of that social media time has changed quite meaningfully during the same period.

For example, the amount of time that the average user spends on TikTok has jumped in recent months, with averages for Q1 this year already more than 20 percent higher than the overall average for 2021.

Indeed, TikTok now claims the highest average time per user of any of the large social platforms, with users spending almost a full day each month using the platform during the first three months of this year.

But it’s interesting to note that the motivations for using TikTok are quite different to the motivations we see for the use of platforms like Instagram and Snapchat.

For example, more than three-quarters of TikTok users say they use the service to find funny and entertaining videos, compared with just 16 percent who say that they use it to communicate with friends and family.

And this is quite different to the behaviours that we see on Facebook, where more than 7 in 10 users say that they use the platform to communicate with other people.

So, given these stark differences, does it still make sense for us to compare platforms like TikTok against platforms like Facebook, especially when it comes to building a marketing plan?

Ultimately, “social” is a behaviour, not a channel, and these latest user trends suggest that each of the top platforms now occupy quite different functional and emotional spaces in people’s lives.

As a result, I think it may be time for us to recalibrate the way we talk about “social media”, and also to have a careful think about how we allocate marketing budgets across different kinds of channels.

For example, if most users treat TikTok as an entertainment channel, does it perhaps make more sense to compare it with streaming platforms like Netflix and Disney+ – or perhaps even broadcast TV – rather than with platforms like Instagram?

Now, there’s no “universal answer” here, because the optimum approach to allocating media budgets depends on various things like the brand, the audience, and the campaign objective.

However, the broader takeaway here is that we should endeavour to divide our media budgets based on what unites the audience.

In other words, we should allocate our media spend based on the motivations and desired outcomes that attract audiences to particular channels, rather than based on somewhat arbitrary media “buckets” like “social media”.

But returning to my conclusion from the previous section, it’s worth noting that an increased focus on “tangible value” is also reshaping how people spend their money, not just how they spend their time.

#4: The rise and fall of NFTs

Now, you may remember that this time last year, NFTs were one of the hottest topics in digital, and they were all over the mainstream news too.

As a result, most people are now aware of NFTs, with a recent GWI Zeitgeist study revealing that more than 2 in 3 working-age internet users have at least now heard of the term.

However, the same research also reveals that fewer than 3 in 10 of us actually know what an NFT is.

More than a quarter of respondents thought that NFTs are a form of cryptocurrency, and even a meaningful share of those who claimed to “understand” NFTs also chose this option.

So, it seems likely that less than a quarter of internet users actually know what NFTs are, despite ubiquitous media hype and billions of dollars of investment.

But let’s stick with those billions of dollars of investment for a moment, because they’re part of a much more alarming set of findings.

To start with, data from NonFungible.com reveals that the number of wallets trading NFTs each month has tumbled by more than 80 percent since the peak back in December of last year, with fewer than 200,000 wallets trading NFTs over the past 30 days.

To put that figure in perspective, the number of wallets trading NFTs over the past month is 2,385 times lower than the number of unique visitors to yahoo.com, and 600 times lower than the number of teenagers who saw an ad on Facebook.

In other words, NFTs appear to be a lot less popular than media coverage might have you believe.

And moreover, the combined monthly value of NFT trades has fallen by more than 90 percent since the peak in September 2021.

But that’s still not the scariest finding in NonFungible’s data

The company also reports that more than half of the value of NFT trades in the first three months of 2022 could be attributed to “wash trading”.

Wash trading is a practice whereby the same trader simultaneously buys and sells an asset that they already own, in order to artificially inflate that asset’s perceived value.

As an example, you can see that this Loot bag – which NonFungible.com reports was one of last month’s most valuable NFT trades – has been repeatedly traded between the same 2 wallets, over and over again.

And in fact, despite being traded a total of 448 times so far, this particular NFT has only ever had 4 unique wallet owners.

So, even if the NFT market may look like it offers the potential for valuable investment, the data suggests that much of that purported value may in fact be just smoke and mirrors.

As a result, we’re going to need to move quickly away from scams and novelty – and deliver much greater utility – if we’re to see NFTs fulfil their potential in 2023 and beyond.

#5: Will crypto go mainstream?

However, a quite different scenario is playing out in the world of cryptocurrencies, even if there’s plenty of pain for investors here too.

And the first piece of good news here is that the number of people who say that they own some form of cryptocurrency has jumped by more than 50 percent over the past year.

Data from GWI shows that roughly 1 in 8 working-age internet users around the world now owns at least one type of cryptocurrency, with that figure rising to roughly a quarter in Turkey.

However, just as we saw in the previous section about NFTs, speculation and scams continue to distract from crypto’s true potential.

Now, it’s important to acknowledge that most types of investment have taken a nasty hit over recent months.

But the decline in the value of cryptocurrencies has been particularly sharp.

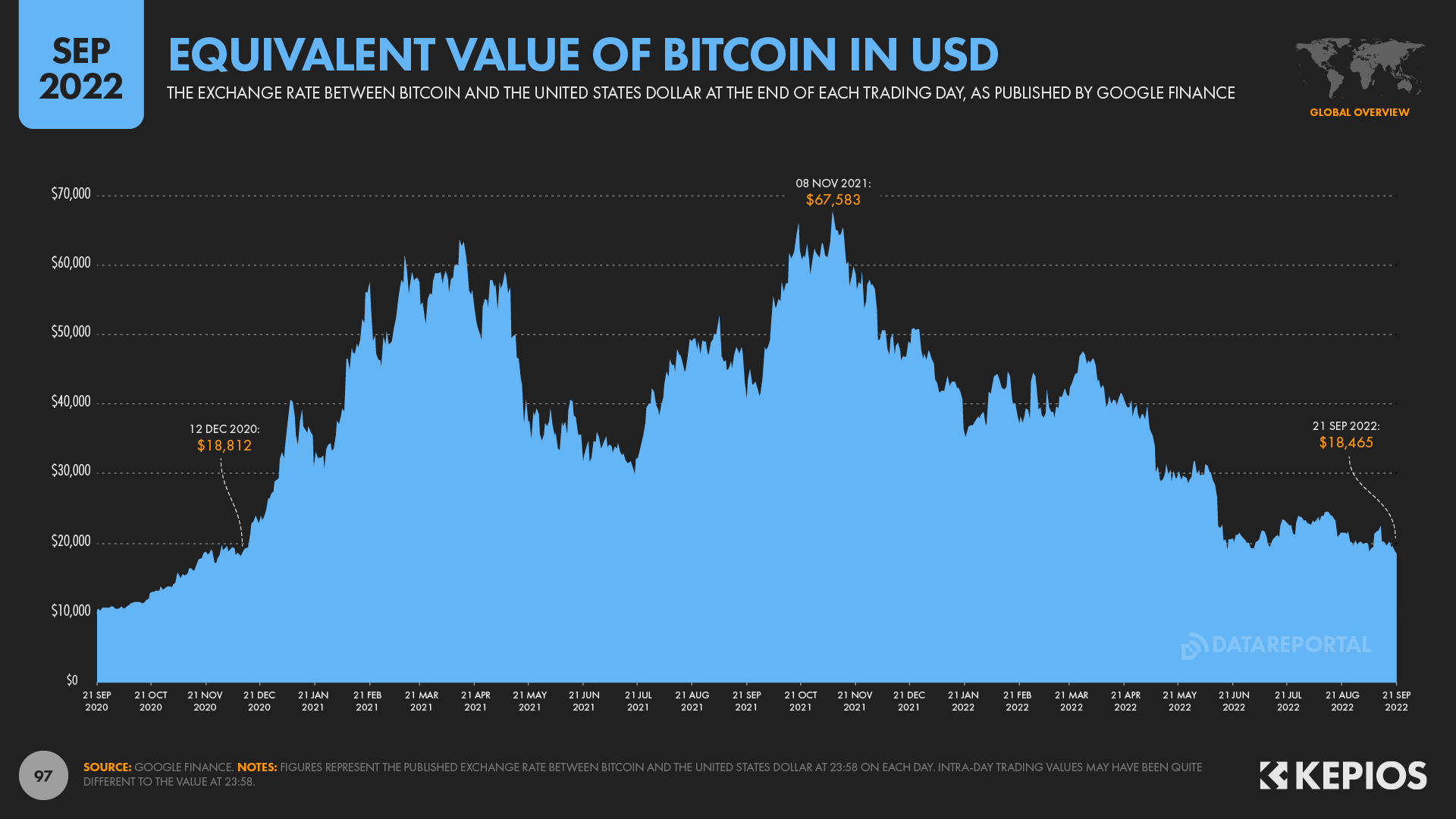

For example, Bitcoin lost 73 percent of its total book value between the 8th of November 2021 and the 21st of September 2022.

And as the trend line in this chart demonstrates, the value of cryptocurrencies also remains highly volatile.

Indeed, the day-to-day Bitcoin-USD exchange rate fluctuated by more than 5 percent on no fewer than 119 separate days over the past 2 years.

Despite its precipitous drop, however, the value of Bitcoin on the 21st of September this year was still 77 percent higher than it was two years prior, so the investments of long-term “HODLers” should still be well up.

But what does the future hold?

Well, various data points indicate that cryptocurrencies continue to attract new investors, and as a result, I think it’s safe to say that cryptocurrencies are here for the long run.

However, with continuing wild fluctuations in value, it’s unlikely that we’ll see many merchants accept cryptocurrency as payment for everyday goods and services any time in the near future.

But seeing as we’ve already covered NFTs and crypto, it only seems right that we now turn our attention to another of this year’s hottest digital topics: the “metaverse”.

#6: The state of the metaverse

And the surprising story here is that – despite widespread scepticism – there is in fact already plenty of evidence to demonstrate the appeal of virtual worlds.

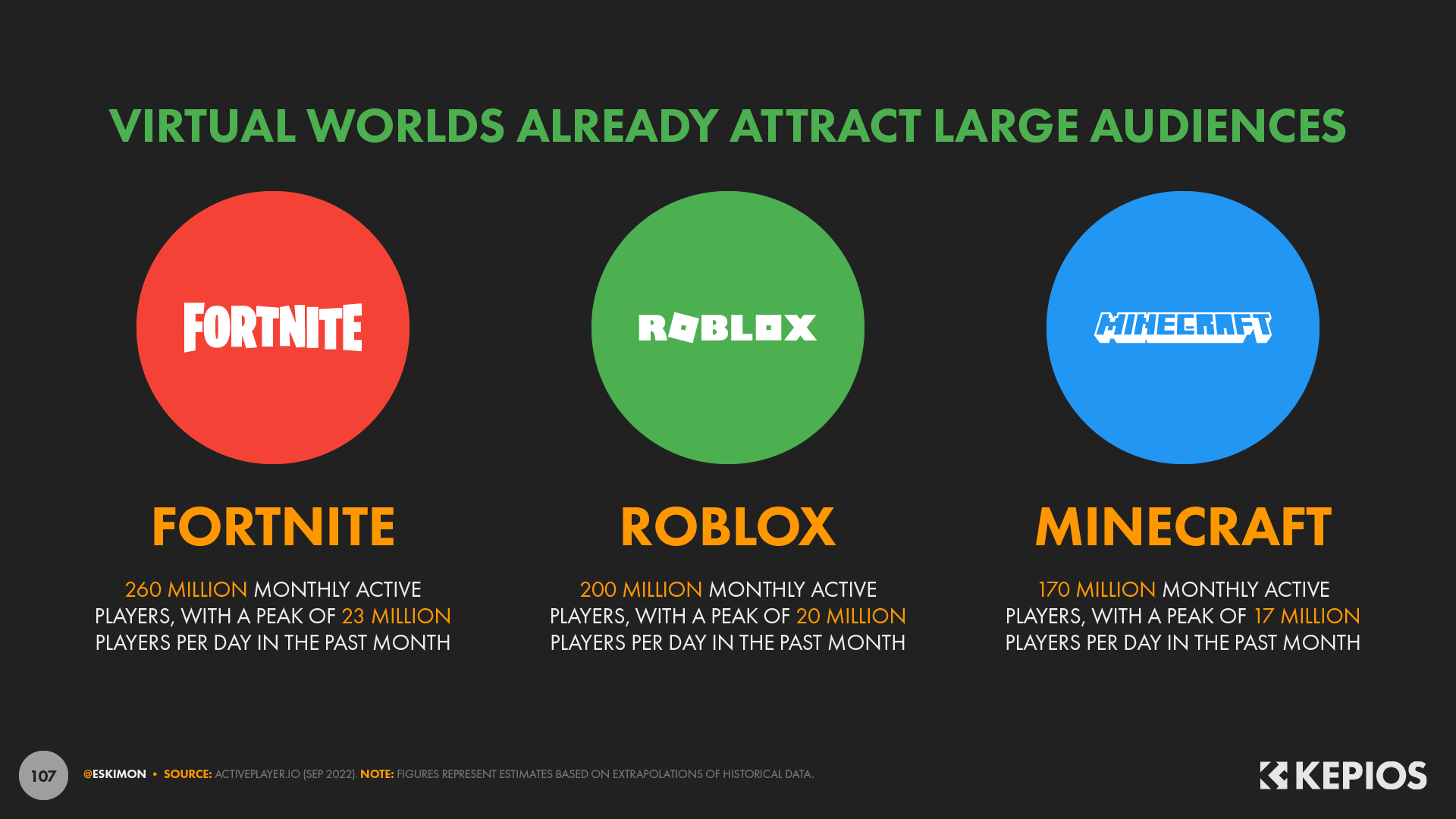

For example, analysis from ActivePlayer.io suggests that more than a quarter of a billion users play Fortnite each month, with upwards of 20 million users playing every day.

And ActivePlayer’s analysis suggests that other worlds are attracting huge user bases too, with Roblox seeing roughly 200 million monthly active players, and Minecraft close behind at 170 million monthly actives.

However, at least for now, the data all seems to point towards a clear trend, and that’s that the metaverse is still synonymous with gaming.

But that isn’t necessarily a problem, because – despite stereotypes – video games remain popular across all demographics.

Now, admittedly, the kinds of games that are popular in each of these cohorts varies considerably.

But nonetheless, the data clearly shows that video games are already hugely popular across genders and age groups.

For example, roughly two-thirds of women aged 55 to 64 say that they’re gamers.

And people spend a lot of time playing games too.

Research from GWI shows that – on average – working-age internet users spend more than an hour per day playing on a games console, and that doesn’t include the time that they spend playing games on other devices like smartphones.

And in more good news for metaverse advocates, there’s plenty of evidence to suggest that in-game experiences can also be highly appealing.

For example, 12 million users attended the first day of Travis Scott’s “Astronomical” event in Fortnite in 2020, while Marshmello’s 2019 Fortnite gig attracted close to 11 million people, well before COVID-19 made virtual events the norm.

However, there’s precious little evidence to suggest that virtual business meetings with avatars cut off at the waist will catch on any time soon.

So what does the future hold for the metaverse?

Well, based on the available data, Kepios analysis suggests that virtual worlds need to offer something distinct to the real world if they’re to gain momentum and traction.

Indeed, many people are drawn to virtual worlds because they hope to escape reality, and I suspect that current efforts to recreate real-world environments – especially physical-world stores – may be missing the point, as well as the metaverse’s real potential.

And moreover, trends suggest that it may take quite some time for the appeal of the metaverse to extend beyond its current gaming focus.

So, for the next section, let’s change gears a little bit, and turn our attention to more immediate opportunities.

#7: The truth about Facebook’s “demise”

And let’s start with one of the most pervasive myths in digital: the idea that “Facebook is dying”.

Now, to be clear, this isn’t a new story.

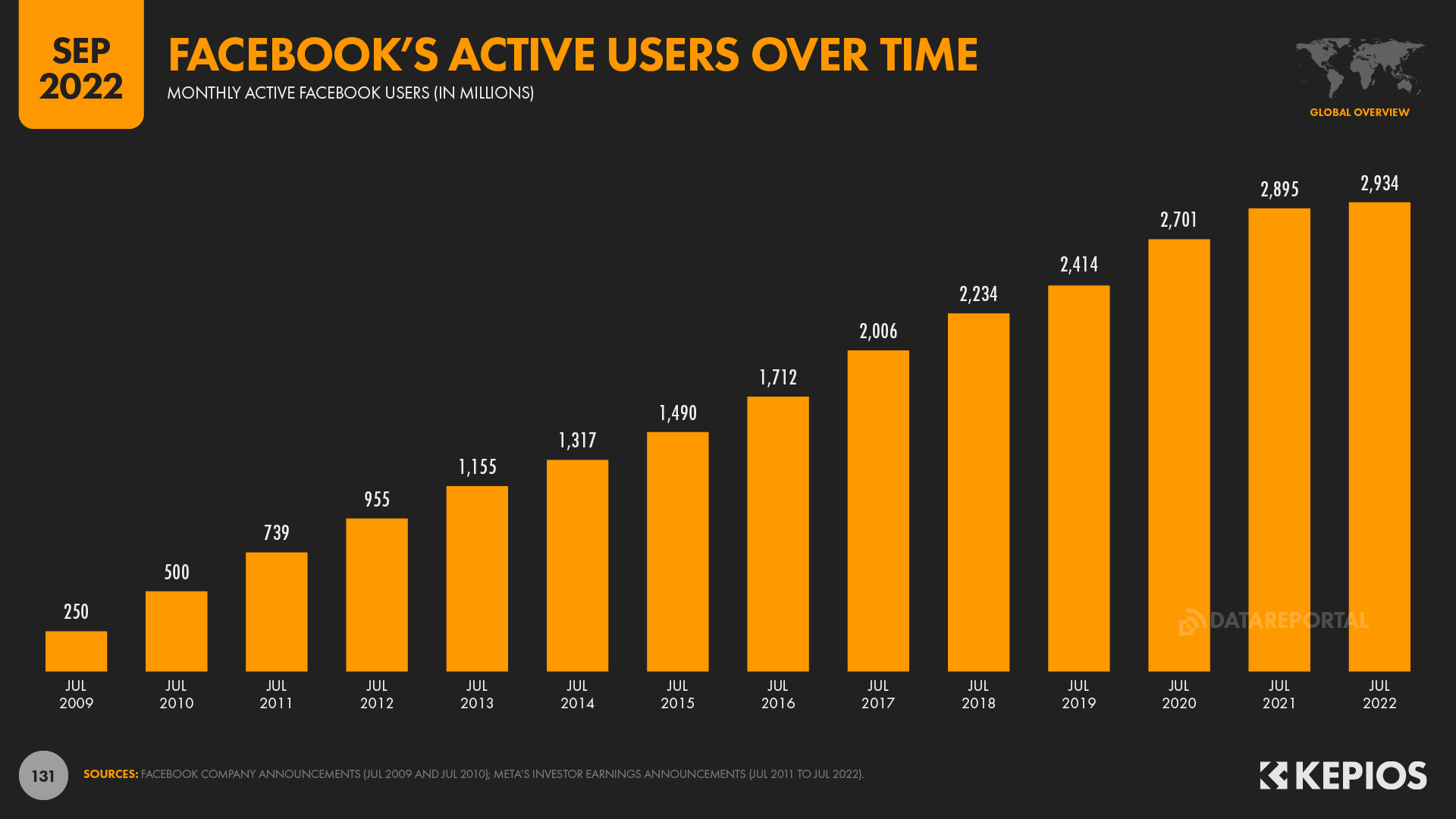

Indeed, a New York Times headline decried a “Facebook Exodus” way back in 2009, since which time Facebook’s active user base has increased by a factor of more than 10.

But – somewhat inconveniently for the media – the latest data still don’t corroborate the idea that Facebook is dying.

And in fact, Facebook still has the largest active user base of any social media platform in the world, with almost half a billion more users than its next nearest rival.

And while Facebook’s global monthly active user count did fall by 2 million in its Q2 2022 earnings announcement, our analysis suggests that this drop was largely – if not entirely – the result of US sanctions on Russia.

Perhaps more tellingly though, there are various third-party data points that demonstrate the ongoing vitality of the Facebook platform as well.

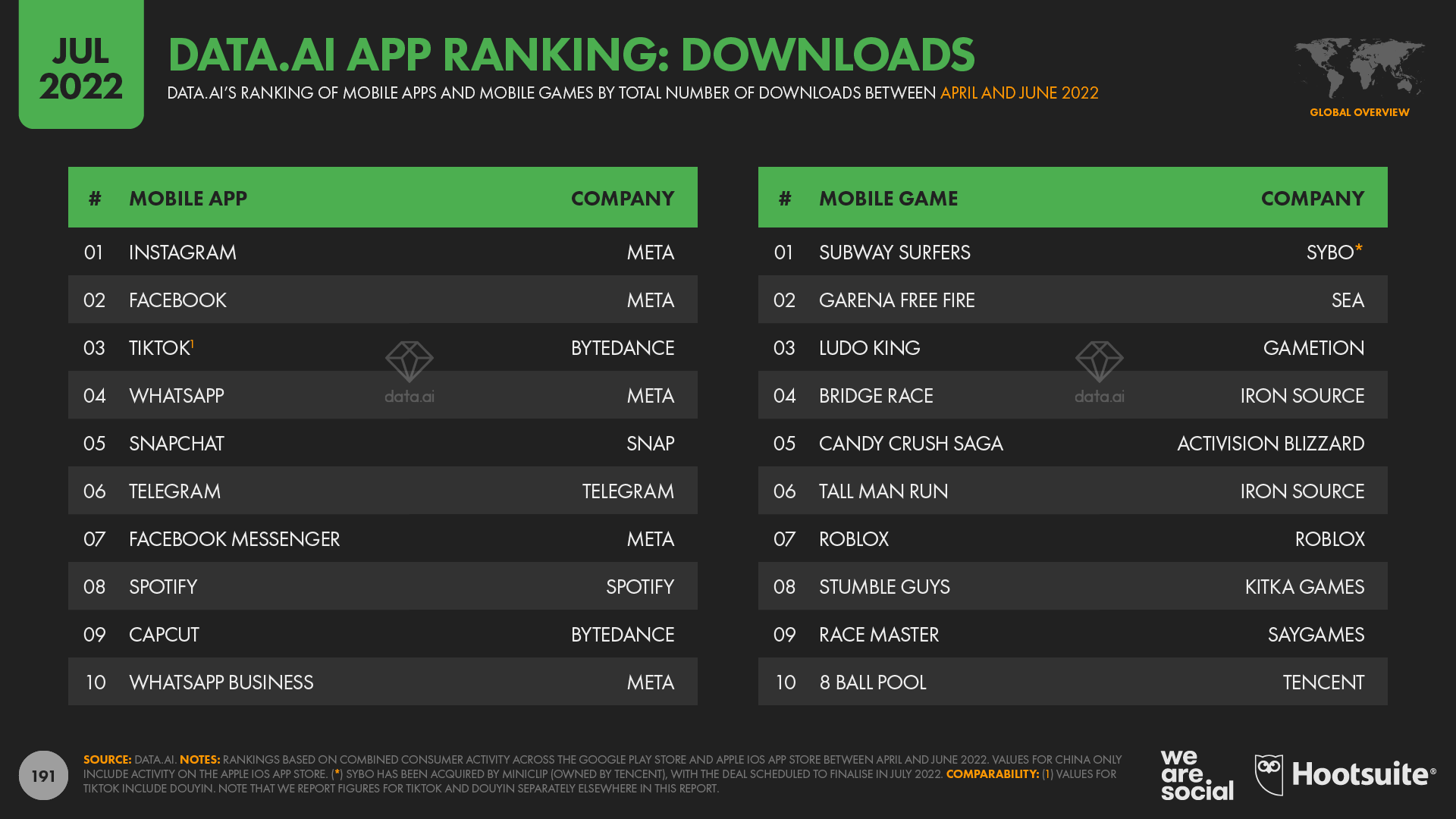

For example, data.ai reports that Facebook still has the largest active user base of any non-game mobile app in the world.

And similarly, GWI’s latest research shows that Facebook retains third place in the global rankings of people’s “favourite” social media platforms.

But what about those younger audiences – surely the kids have all abandoned Facebook by now?

Well, sure enough, there is evidence to support that argument.

For example, you may have seen a variation of this Pew Research chart floating through your social feeds recently, which shows that the use of Facebook amongst US teens has dropped by more than half over the past 7 years.

However, other data shows that – at a worldwide level – 1.35 million more teenagers saw a Facebook ad in June 2022 compared with April 2022.

In other words, Facebook’s global teenage user base continues to grow.

So what’s actually going on?

Well, it’s critical to note that Pew’s research only covered teens in America, and while we may see some parallels in Western European countries, US trends are not reflective of those we see at a global level.

Indeed, Kepios analysis reveals that US users make up less than 10 percent of Facebook’s global active user base.

So, while Zuck and team will certainly be worried about those US trends, global data suggest that Facebook is in fact still gaining teenage users, not losing them.

And the key takeaway here is that Facebook remains a hugely valuable opportunity for marketing.

Sure, the way people use Facebook continues to evolve, and it may not be as “sexy” as it used to be, but there’s very little evidence to suggest that Facebook will “die” anytime soon.

And to support that argument, I’d like to draw your attention to the latest web traffic figures for Yahoo! from Semrush, which show that the platform continues to attract roughly half a billion unique visitors every month.

Based on this precedent, even if Facebook were to slip from the top of the rankings in the coming months, there’s plenty of evidence to suggest that its appeal will endure for many years to come – and certainly well beyond 2023.

So the broader takeaway from this section is that we need to be careful not to get distracted by media click-bait.

We always need to do proper due diligence, and use a range of the latest data to help us understand what our audiences are really doing online.

And the good news is that our free Global Digital Reports will continue to help you identify those behaviours, with data for every country in the world except North Korea and the tiny island of Pitcairn.

#8: Tips for TikTok success in 2023

However, even if Facebook is still top dog when it comes to social media reach, it’s clear that TikTok has been gaining rapid momentum over recent months, so let’s take a closer look at how to make best use of TikTok in 2023.

And to kick things off, it’s worth highlighting that – around the world – TikTok now reaches more than a billion adults aged 18 and above each month.

TikTok’s active user base is still growing quickly too, with our latest analysis indicating that the platform’s adult user base grew by more than 5 percent in the three months between April and July 2022.

And TikTok isn’t just growing its active user base, either.

As we saw earlier, TikTok now enjoys the highest average time spent of any of the large social platforms.

So, with impressive numbers like these, it’s easy to understand why there has been some much hype around TikTok in the media, and in the marketing industry.

But here’s where things start to get interesting.

Because other platforms may already be stealing some of TikTok’s thunder.

For example, Kepios analysis reveals that Telegram may be growing even faster than TikTok.

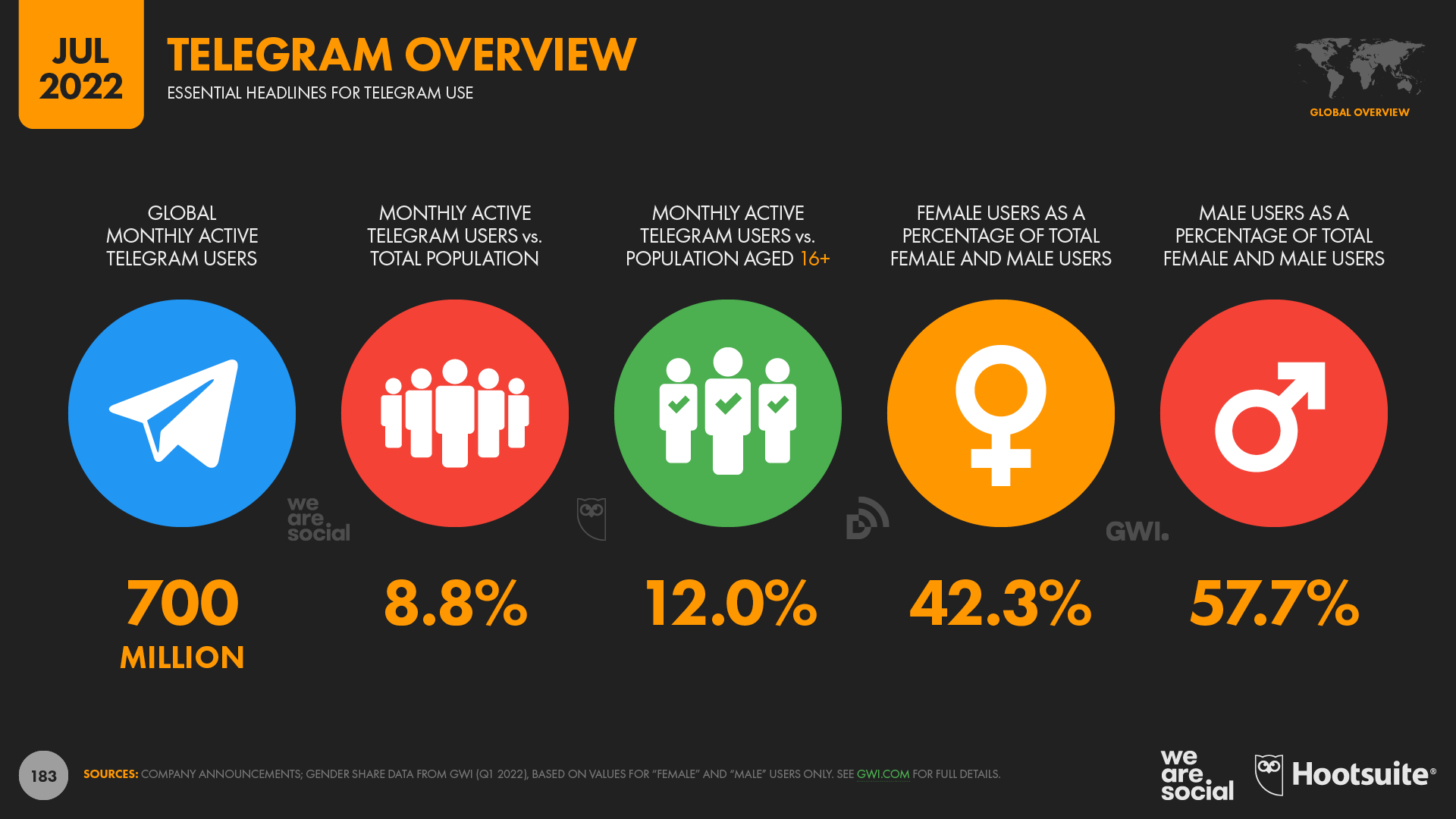

The messenger platform’s latest user update indicates that it has added more than 200 million monthly active users over the past 18 months, taking its global total to 700 million.

However, that’s not the biggest Telegram stat in today’s presentation.

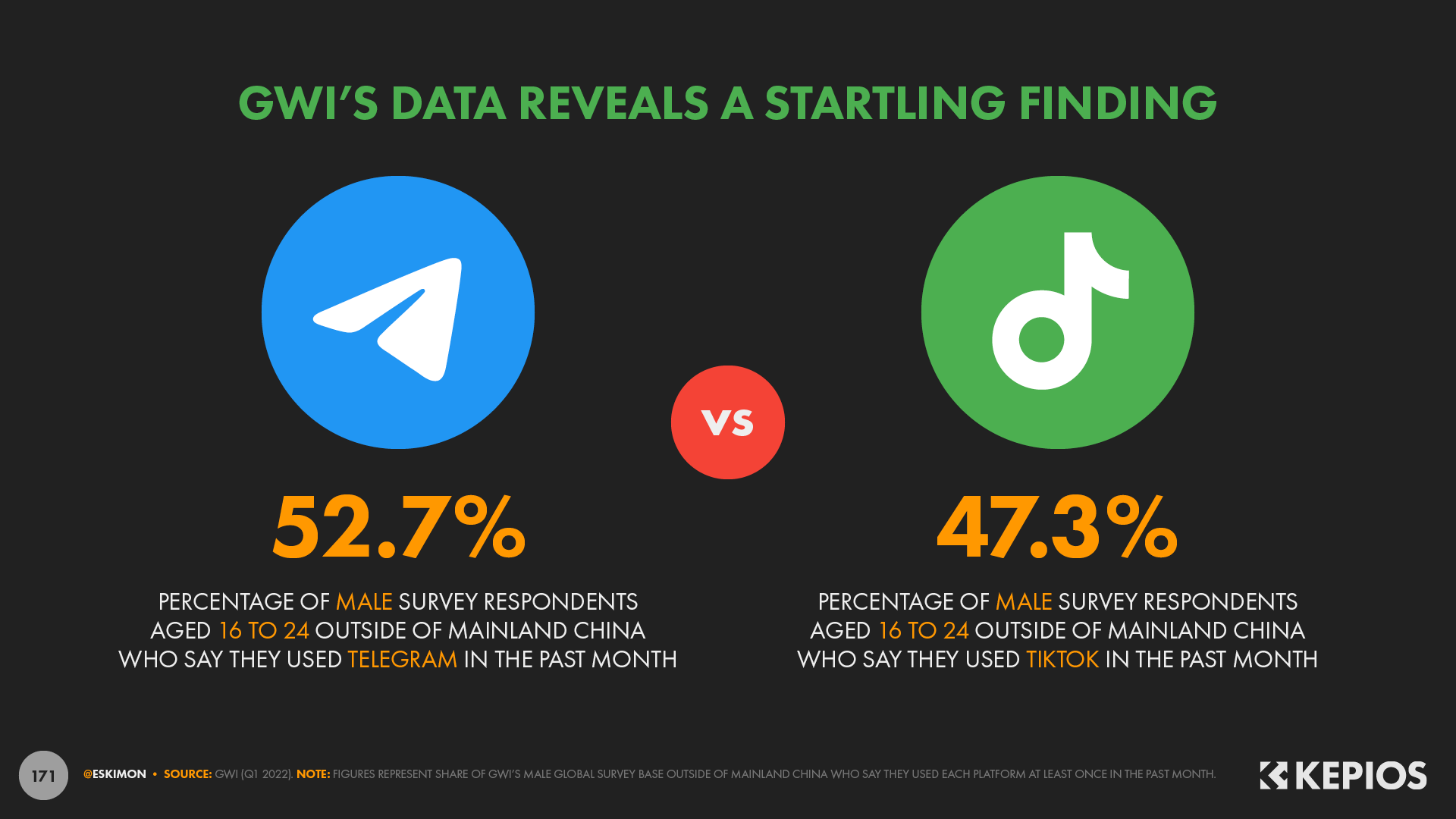

In a truly startling development, GWI’s latest data suggests that males between the ages of 16 and 24 are now more likely to use Telegram than they are to use TikTok.

Now, it’s important to stress that this data is based on self-reported usage, and is restricted to the 48 countries covered in GWI’s survey, so it may not reflect the numbers that the platforms themselves would report.

However, these trends suggest that – despite its impressive ascent – TikTok is neither the biggest, nor the fastest-growing, nor the most global digital platform.

Moreover, GWI’s research reveals that marketers can reach more than 99.9% of all TikTok users on at least one other social platform.

And in another surprising finding, GWI’s data also shows that 84 percent of TikTok users between the ages of 16 and 64 also use Facebook each month.

So should marketers still be excited about TikTok?

Well, yes – they absolutely should.

While its reach and growth are undoubtedly important, TikTok’s real “magic” lies in its distinct usage context, and especially in its unique creative opportunities.

So, in order to get the best results from TikTok in 2023, my advice is to focus on creativity, and ensure you’re delivering highly compelling – and truly entertaining – content.

But those Telegram stats I just shared point to the growing importance of messengers overall, so let’s take a closer look at this important trend in our next section.

#9: The outlook for messenger marketing

First up, with the platform now boasting 700 million monthly active users, Telegram’s Channels are an increasingly compelling opportunity for marketers.

Critically, in contrast to group chats on platforms like WhatsApp or Facebook Messenger, Telegram Channels are not subject to follower limits.

Furthermore, only admins can publish content to a Channel, although the Channel’s followers can still react to and comment on Channel posts.

Perhaps most importantly, however, Telegram Channels don’t face the same algorithmic challenges that brands face in other social media feeds when it comes to delivering content to their audiences.

Telegram is still a very busy environment though, so attention and engagement aren’t guaranteed.

However, given its rapidly growing user base and unique service propositions, Telegram clearly offers some compelling opportunities for brands in 2023.

But Telegram isn’t the only messenger platform that’s been seeing impressive growth.

Recent analysis from data.ai reveals that WhatsApp’s Business app was one of the 10 most-downloaded mobile apps in Q2, meaning that the platform now has two apps in the global top 10.

And to put that achievement in perspective, data.ai reports that there are currently more than 4 million apps available for users to download across the Google Play and Apple iOS app stores.

But larger brands will likely use more sophisticated systems for engaging through messenger platforms rather than asking teams to use an app on a smartphone, so it’s likely that most users of WhatsApp’s Business app fall into the small and medium-size business category.

However, this in itself reveals an important finding.

If smaller businesses are indeed embracing messenger platforms for customer service, marketing, and more, there’s a good chance that these activities will influence consumers’ expectations for bigger brands too.

And as a result, there’s a good chance that messenger platforms will finally play a more central role in the marketing mix in 2023.

#10: The rise of wearables

But let’s change gears again for the next section, and shift our attention to wearables, which may turn out to be one of the most influential categories in connected tech in 2023.

And the reason for this is that the number of people who own a smartwatch has jumped by 60 percent over the past two years.

To put that growth in context, the number of adults around the world who own a device like a Fitbit or an Apple Watch is now greater than the number of adults who own a gaming console.

The rise of these connected wearables has particular implications for digital healthcare, which is one of the industries that we expect to see deliver important growth and innovation in the digital world over the coming years.

However, the increasing adoption of smart watch devices may have some important implications for marketers, especially if it results in people spending less time using their phones.

But the future of wearables isn’t just about what’s on our wrists.

Smart glasses are still in their infancy, but they have the potential to revolutionise digital experiences.

And perhaps the most important change here will be the transition to “heads up displays”, which will enable people to engage with connected content without diverting their attention from another activity.

In other words, instead of needing to look at a particular device, the content delivered by smart glasses will become an extra “layer” of our vision, superimposed over the world we see around us.

And as a result, we expect that wearables will bring about the next revolution in connected experiences, delivering a wave of innovation that we last saw with the rise of the smartphone.

#11: Generative A.I. and “artificial creativity”

And talking of “revolutions”, we can expect generative AI to deliver big changes in the year ahead too.

Current trends suggest that the capabilities of tools like Dall•E and Midjourney will continue to accelerate in 2023, and developers report that we’ll likely see functionality for audio and video become more widely available over the coming months as well.

This will almost inevitably bring significant disruption to creative industries.

However, with the existing technology already capable of producing images like this award-winning Midjourney creation from Jason Allen, we anticipate that generative AI will start to reshape everybody’s relationship with creativity over the coming months too.

And with these tools making it easier for anyone to create beautiful “artwork” in a matter of seconds – from the comfort of their armchair, using just a few text prompts – we may even need to redefine what we mean by terms like “creativity”.

The debate around the role of these tools has already reached fever pitch, but it seems likely that it will only intensify in 2023.

Whatever your take on these technologies though, the genie is already out of the bottle.

As a result, it’s up to us as individuals to decide whether we want to embrace generative AI, or to engage in what will likely be a futile battle against it.

#12: Self-sovereign identity

And to finish up today’s session, let’s turn our attention to the next wave of blockchain innovation.

With ongoing concerns around online security and privacy, the ability to own, manage, and use our digital identity is increasingly important.

“Self-sovereign identity” promises to make that possible, enabling individuals to build their own, secure online ID that they can use across the gamut of connected services and devices.

Indeed, SSI has the potential to become omnipresent in our digital lives.

For starters, an SSI solution would simplify everyday activities such as logging into all of our digital services, and applying the same set of preferences across all of them.

However, SSI would enable us to securely store and manage more sensitive data too, offering much greater freedom and flexibility when engaging with healthcare and financial services.

And in the longer term, there’s a good chance that SSI will become the definitive form of ID in all aspects of our lives, even replacing national ID cards and passports.

And the exciting news is that various SSI initiatives are already active, including Tim Berners-Lee’s SOLID specification, the Sovrin Network, and the European Union’s Blockchain Services Infrastructure.

Various barriers remain though, especially when it comes to commercial aspects and issues of state sovereignty.

As a result, the promise of universal self-sovereign identity is still a long way off.

However, we can expect these initiatives to continue gaining investment and momentum in 2023, and it seems almost inevitable that some form of SSI will become a part of our everyday reality at some point in the future.

Wrapping up

That’s all we have time for in today’s presentation though, because I want to leave plenty of opportunity for Q&A.

However, remember that you can dig deeper into almost all of the stats that I’ve shared with you today – as well as thousands more charts exploring the world’s evolving digital behaviours – over on DataReportal.com

And if you’d like to get in touch with me after today’s session, here are a few of the ways that you can do that.

But with that, let’s move on to our Q&A… […and if you have a question for me after reading this transcript, please pop that in the comments below, or share it with me on Twitter or LinkedIn.]

Click here to see all of Simon’s articles, read his bio, and connect with him on social media.